Loan amount

The dollar amount you want to borrow. When you enter a loan amount, requesting only the amount you need generally lowers the monthly loan cost and reduces total interest.

Before you apply, use this personal loan payment calculator to compare personal loans, enter a loan amount, choose a loan term, and see a monthly estimate for illustrative purposes.

Adjusting the numbers takes seconds, and it costs nothing to explore scenarios. The tool is for planning, not a loan offer. Your actual personal loan rate, APRs, fees, maximum loan you can receive, and terms depend on state rules, credit history, creditworthiness, the product you apply for, and the agreement you review if Avio Credit can extend an offer.

Adjust the amount and term to compare a monthly estimate, total amount, and finance charges before you apply.

Your actual rate may vary by state, loan product, and borrower profile.

The dollar amount you want to borrow. When you enter a loan amount, requesting only the amount you need generally lowers the monthly loan cost and reduces total interest.

The number of months over which you would repay the loan. A shorter term can mean a higher regular bill but less total interest. A longer term may lower the monthly figure but increase the overall cost.

The yearly cost as a percentage, including interest and, when applicable, fees. Rates range by state, product, and applicant profile; your agreement explains whether the final rate includes fees and other charges.

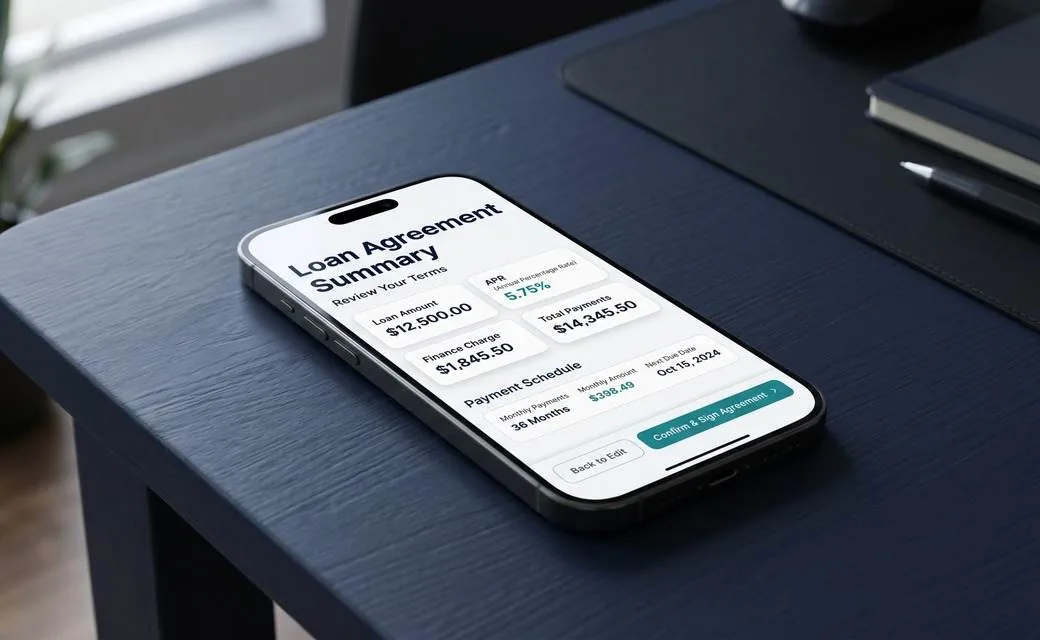

What a single bill might look like under those inputs. For installment loans, amounts are typically fixed and scheduled on regular dates.

The sum of principal and interest payments over the life of the loan. It is different from the amount you borrow and can be easier to review in an amortization schedule.

The difference between the total paid and the amount financed. This shows the annual cost and dollar cost of borrowing money above the principal.

Complete the secure online form in just a few minutes. Review your actual rate, fees, schedule, and disclosures before you accept any loan agreement.

Start Your Application

You complete an online application with personal, income, banking, and checking account information. The application is submitted directly to Avio Credit for review.

Avio Credit may review your credit history, income, banking activity, and other application data as part of the underwriting process. The specific factors reviewed can vary by product and state. Submitting an application does not guarantee approval.

If your application meets eligibility criteria and is approved, you'll receive a loan agreement that includes your actual rate, finance charge, amount, schedule, and all fees. Read this document carefully before accepting.

For approved borrowers who accept the loan agreement, funds are deposited via ACH to the bank account on file. Funding timing depends on when final approval is completed, your bank's processing schedule, ACH cutoff times, and whether the funding date falls on a weekend or holiday. Funds may be available as soon as the next business day for some approved borrowers, but timing is not guaranteed for everyone.

Debits are typically scheduled via ACH on dates established in your loan agreement. Keeping your bank account funded on due dates helps avoid returned payment fees and potential negative credit reporting.

Your schedule, including each due date and amount, will be set out in your loan agreement. Installment loan amounts are typically fixed and generally collected via ACH from the bank account you provided during the application.

Review your due dates against your pay schedule before accepting. If the dates do not align well with when you receive income, contact Avio Credit support before accepting the loan to understand your options.

APR expresses the yearly cost as a single percentage, making it easier to compare loan options. For short-term and small-dollar loans, the percentage can appear high even when the total dollar cost is modest, because the payoff period is short.

Before accepting any loan, compare the rate and the total finance charge - the actual dollar amount you'll pay above the principal. Rates, fees, and available amounts vary by state, product, and borrower profile. Exact costs are disclosed in your loan agreement before funding.

Paying off your loan ahead of schedule may reduce the total interest you pay. Whether early payoff is permitted without penalty depends on your loan agreement and state law, so check your agreement for any prepayment terms.

If a scheduled debit cannot be collected because of insufficient funds, a closed account, or another reason, you may be charged a returned payment fee or late fee. Delinquent accounts may be reported to consumer reporting agencies, and persistent non-payment may result in collection activity and additional costs.

If you anticipate difficulty with an upcoming debit, contact us before the due date. Early communication gives you more options.

Request only the amount necessary to cover the immediate need. Matching the amount you need to clear financial goals can help keep the total interest lower.

Add the estimate to fixed expenses like rent, utilities, insurance, and credit card debt. If the total strains your income, consider a smaller loan or another option.

A longer term reduces the monthly figure but increases the total amount you'll pay. Make sure you can make payments across the full timeline, not just the first due date.

Depending on your situation, other options may cost less: an arrangement with a creditor, an employer payroll advance, a credit union loan, a secured credit card, or assistance programs in your area. Visit Alternatives to see a broader list.

Once you accept a loan offer and funds are disbursed, you are responsible for the terms as written. Review the rate, finance charge, schedule, and all fee disclosures before you click accept.